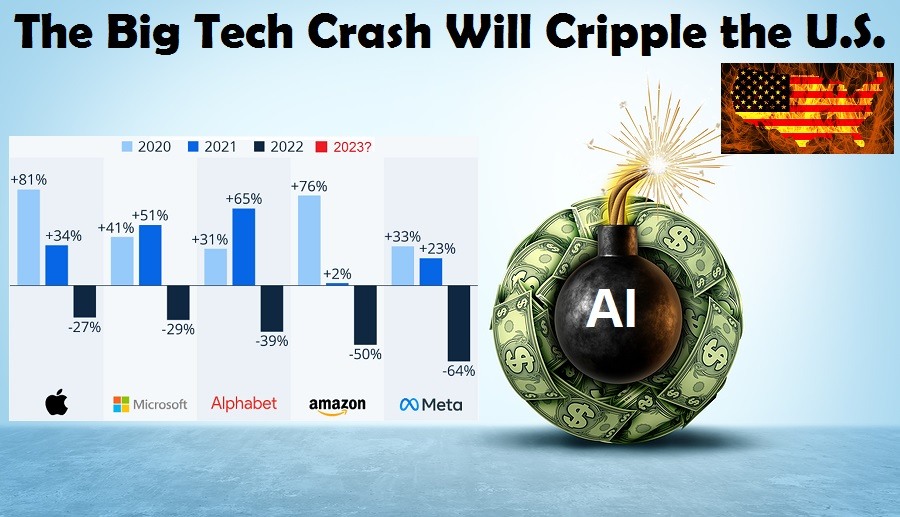

Big Tech is Rushing to Bankrupt America – Investing in a Science Fiction View of the Future is Going to End and We will All Suffer

With new IPOs coming up for Musk's SpaceX and for Sam Altman's OpenAI, Wall Street, which is increasingly becoming less tech savvy and just investing in hype, is going to take the next step in bankrupting America. Haven't people learned from Elon Musk's constant lies for the past two decades? Where are his fully autonomous driverless taxis? Where are the $35K human robots that he promised would be in everyone's homes by now? It's all BS! But people keep feeding it, too scared to be left behind. Now the biggest IPO in the nation's history is set to happen next week for SpaceX. Is SpaceX rolling in the cash with record sales? Nope. It is actually losing money. So why will Wall Street groupies invest? Because Musk promised them there would be floating data centers in space to fuel the expansion of AI, in the future. Everyone and anyone who is investing in Musk is continuing to invest in the future, for a version of science fiction which will never happen. And because Musk is also behind removing regulations to protect Americans' retirement accounts from such risky investments, within the next few weeks a majority of American's retirement accounts may be left holding the bill for these mammoth Big Tech IPOs, whether they want to or not. They say Rome did not fall in one day, but America just might.